Ryan Pleggenkuhle

Ryan Pleggenkuhle

3 min read

Navigating the End of the Penny: What it Means for You

Rethinking Change: Navigating the Penny's Discontinuation Why is the penny being retired?The main reason is the high manufacturing costs of...

Big banks are turning away small businesses.

According to a recent Financial Brand article, big banks are approving just 13% of small business loan applications, leaving many entrepreneurs searching for alternatives to fund their dreams.

That’s where you, as a community-based financial institution, come in as the hero, championing local small and mid-sized businesses (SMB) while expanding your loan portfolio along the way.

And now, the U.S. Small Business Administration (SBA) has introduced a new friend to help you do just that.

Launched on Oct. 1, 2025, MARC is a lending product offering working capital — up to $5 million — for small businesses in the manufacturing sector.

Funds can be used in tandem with other SBA and conventional commercial loans to support operational needs, such as working capital, inventory purchases, or new projects. There is no down payment requirement (NOTE: This can vary by lender).

What do you notice?

Issue #1: Since this is a tiered account, this ad needs to include the balance requirement to earn the APY and it must be in close proximity to the APY.

Reg. DD requires the corresponding minimum balance to be included in close proximity to the APY for each tier. (Note: You can highlight one tier and its corresponding balance — the rest can be included in your disclosure.)

Issue #2: When seeing the ad, it appears that anyone could open the account and get this rate. However, this account has three qualifications the customer must meet every month to receive this APY.

Our Recommendation for #1 and #2: Under the 2.01% APY add something like: “On balances up to $____ when you meet qualifications.” Another option: “On balances up to $______. Terms apply.” This lets the reader know that there are qualifications. Then they can get details one click away.

Additional Insights:

According to the SBA, MARC is the first-ever loan program specifically designated to support America’s small manufacturing operations (fewer than 500 employees), which make up 98% of all U.S. manufacturers.

The SBA notes, in addition to offering working capital for small manufacturers, MARC is “specifically designed to provide maximum flexibility and minimal red tape.”

While approval rates for small business loans have dropped at the largest banks, new businesses continue to grow, with “400,000 to 450,000” new applications coming in each month since 2020, according to the Financial Brand.

With MARC added to the SBA’s roster, your FI may be well-positioned to fill in the SMB lending gap.

3 min read

Rethinking Change: Navigating the Penny's Discontinuation Why is the penny being retired?The main reason is the high manufacturing costs of...

2 min read

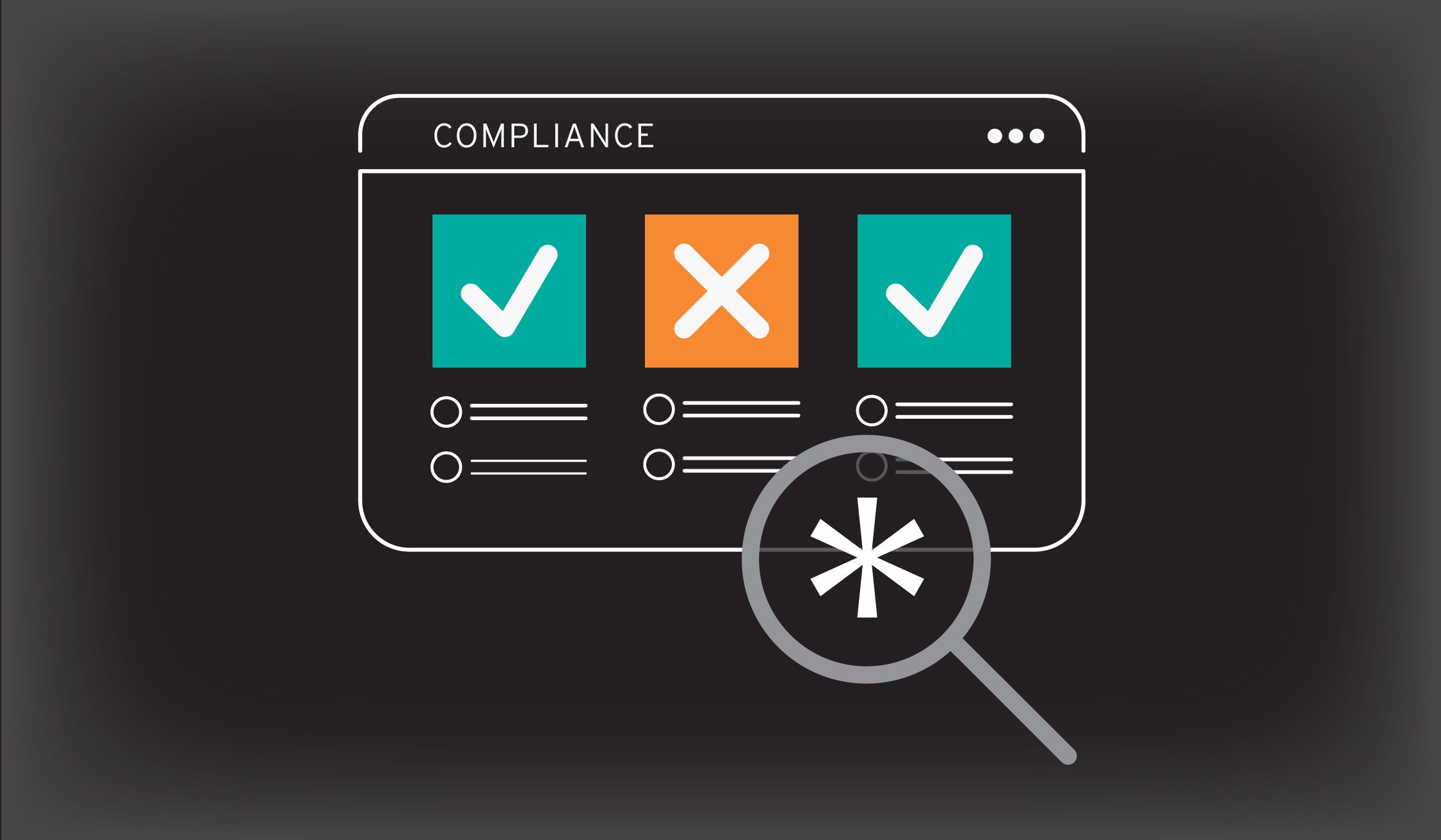

Over the years, digital advertising has grown and so have compliance challenges. Many regulations have not been modernized to reflect the digital...

3 min read

Note: This article was written featuring insights from Becki Drahota, Mills CEO. Considering a merger or acquisition? You’ll need the recipe for...