Crystal Steinbach

Crystal Steinbach

3 min read

Don’t Fall for the “Deepfake”

Follow these 4 tips to avoid this tricky AI-enhanced scam. Are you familiar with the term “deepfake”? No, it’s not a schoolyard football play drawn...

Research has shown that complicated checking accounts are both difficult to sell, and unattractive to consumers. The packaging of “perceived” benefits, including rewards, is not enough to catch someone’s attention and motivate them to move. In today’s marketplace, to entice a consumer to switch takes 1) simplicity, 2) differentiation, and 3) relevance.

Consumers “come” to a bank for convenience, and they “stay” for service. Your deposit product mix must meet the needs of the consumer at both ends. And, if that wasn’t enough, your products are measured internally by profitability.

When it comes to deposit acquisition and retention, it’s imperative that you continually monitor and analyze your banking products and features.

Ready to take your onboarding program to the next level? Contact us today to learn how we can help you strategize, develop and automate a digital onboarding program that sets your bank or credit union apart from the rest.

Now that you’ve identified some important metrics, let’s put them into action to determine profitability. Branches play a key role in deposit growth, in the form of both new customer acquisition and existing customer share-of-wallet.

The overall objective is to increase branch profitability by improving your penetration of the deposit products through a targeted, profitable and desirable product suite delivered by branch personnel, and product specialists, while deepening relationships and improving profitability of the deposit customer base.

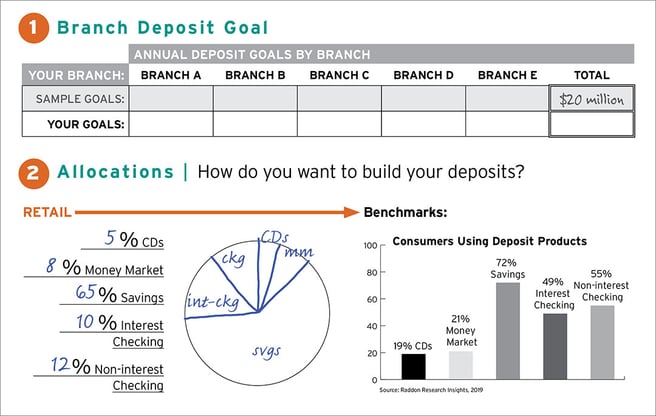

To do this, identify the total annual deposit goals by branch. And remember, these goals are a full team effort – and no one person, department or technology can achieve this goal alone. Using that percentage, determine the mix that will be most profitable and will allow you to reach your deposit goals. Below is an example of documenting your branch deposit goals, and for allocating your deposit product mix.

Source: Raddon Research Insights, 2019

Source: Raddon Research Insights, 2019

Analyzing your products and product features will help you to make informed decisions when it comes to creating strategies for deposit product mix. By evaluating the number of consumers and number of consumers over time by product, and broken down further by product feature, you can better see how consumers needs are being met. You can identify products or features that have come near the end of their lifecycle or that are emerging in consumer interest. I encourage you to further filter the data by various consumer segments such as age range, y group/model, and deposit type.

Mesh this data with the utilization and utilization over time data, and now you can really see what the relationship looks like with your consumers from a product standpoint. I challenge you too, to break down the utilization data into multiple views such as daily utilization by feature – how many consumers are using say mobile bill pay daily, AND how frequently do unique users with access to the feature use bill pay. These metrics will look very different despite how similar they sound on paper (screen?).

You’ve got your data, your goals and objectives, and now you’re putting the data to work. At this point in the process, you’re informed with powerful, indisputable information. But you still need to actually develop your products. And there is one shortfall in using data for banking product development that I want to point out – the data doesn’t help you when it comes to introducing new product features. It can help in tracking and monitoring the adoption or success of that feature, but you’ll need to rely on other methods and take a few risks to ensure that you are always offering your banking customers the services they want or need. As you move forward in developing your products, please take a look at the following considerations. And, as always, we’re here to help!

Remember: Simple. Different. Relevant.

3 min read

Follow these 4 tips to avoid this tricky AI-enhanced scam. Are you familiar with the term “deepfake”? No, it’s not a schoolyard football play drawn...

2 min read

This message may seem out of character, especially to those who know we’re the biggest advocates of data-driven decision-making there is. That said,...

4 min read

Digital solutions to help generate deposits and strengthen your brand From platforms to consumer behavior, the way that you promote your financial...